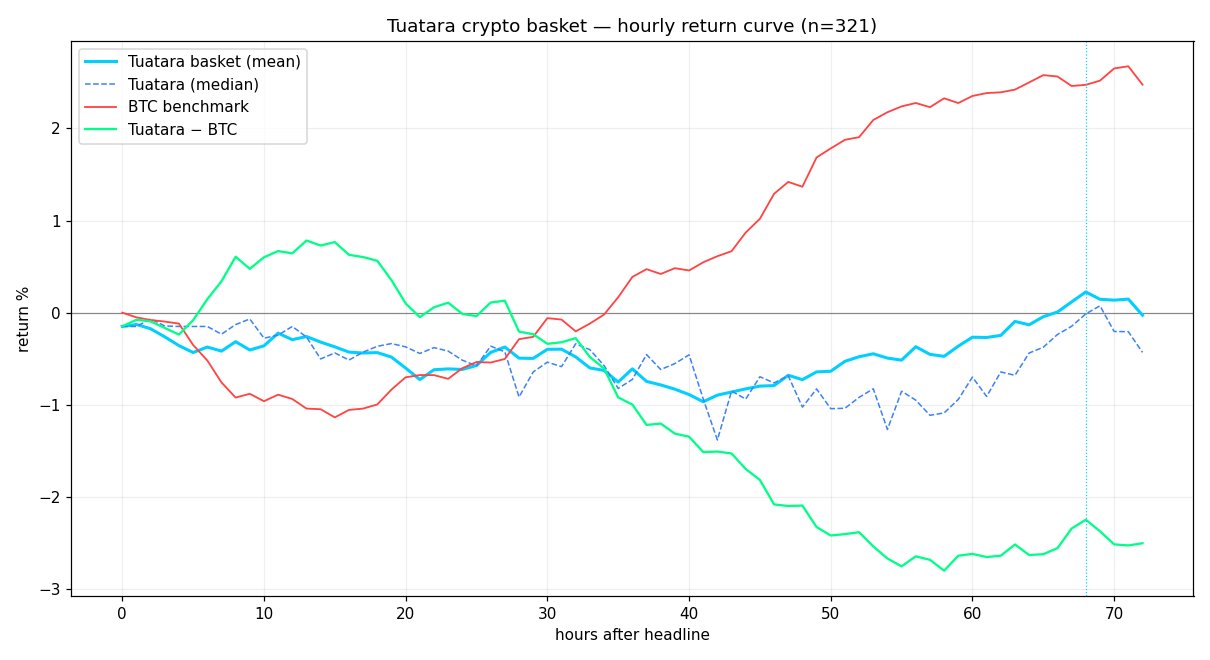

Tuatara Headline Signal — Hourly Return Curve

Equal-weight directional return of the Tuatara vector basket, sampled every hour for 72 hours after a news headline, aggregated across 321 tradeable headlines. Causal entry at the headline timestamp; BTC is the benchmark.

Where the alpha lives. The signal’s edge over the market (Tuatara − BTC, green) is

front-loaded: it peaks at +0.78% around 13 hours and is positive only in the

~6–20 hour band, then decays to −2.5% by 72h as BTC rallies and the basket lags.

For market-neutral / long–short use, the optimal hold is ~12–18 hours, not days — the daily

backtest’s “2–3 day” best hold was capturing BTC beta, not signal.

Return by hold time

| Hold (h) | Basket mean % | vs BTC % | Win % | n |

|---|---|---|---|---|

| 1 | −0.13 | −0.08 | 39.4 | 193 |

| 6 | −0.37 | +0.15 | 44.3 | 192 |

| 12 | −0.29 | +0.64 | 43.8 | 192 |

| 13 ◄ peak alpha | −0.26 | +0.78 | 43.8 | 192 |

| 18 | −0.43 | +0.56 | 45.8 | 192 |

| 24 | −0.62 | −0.01 | 43.6 | 202 |

| 36 | −0.61 | −1.00 | 42.7 | 192 |

| 48 | −0.73 | −2.09 | 41.6 | 202 |

| 72 | −0.03 | −2.50 | 46.5 | 202 |

Method

Cymetica · Tuatara vector research · signal/research only, not investment advice ·

cymetica.com